Meta’s Ad Machine Is Worth $240bn. Now Investors Want to Know What Happens If It Breaks

WARC forecasts Meta's ad revenue will hit $240bn in 2026. The AI flywheel is working. The question investors are asking is whether it can carry the weight being put on it

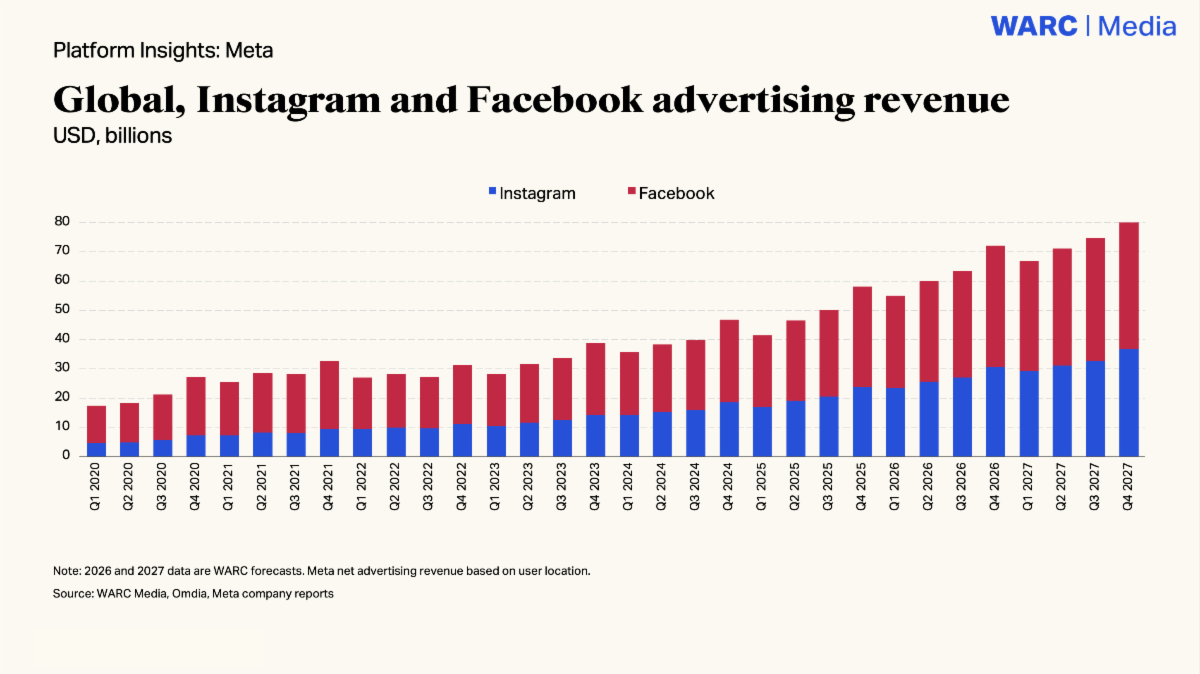

Meta’s advertising business is on course to generate $240bn this year, a 22.3% increase on 2025, according to new research from WARC Media. It confirms Meta’s dominance in social advertising and sharpens a question the company has avoided answering: what happens when a business funds everything from a single revenue stream?

In 2025, Meta’s ad revenue grew 22% to $196bn. Prior to 2023, it had been losing ground: its share of global social spend was declining and annual growth lagged the wider market. The turnaround came through AI. Rather than loading more ads, Meta invested in automated campaign tools and a unified AI architecture that optimised for advertiser conversions without degrading the user experience. The flywheel started turning faster.

Facebook accounts for 60% of Meta’s ad revenue, Instagram 40%. Both are growing at double-digit rates. Kantar analysis suggests the allocation doesn’t reflect the returns: the average campaign puts just 4% of budget into Instagram and 5% into Facebook, yet both platforms over-deliver on brand awareness, association and purchase intent relative to spend. More than 40% of global marketers rank Instagram among the top four platforms for attention.

The CapEx Problem

Meta has announced a $125bn–$145bn increase in annual AI capital expenditure, funded almost entirely through advertising. Unlike Alphabet or Amazon, Meta has no meaningful alternative revenue base. Investors balked: the stock fell 10% after the announcement.

“Meta’s flywheel is spinning faster than ever. The company’s AI-driven automation is transforming how brands connect with audiences, driving rapid growth in advertising spend with Facebook and Instagram. This is enabling further record-breaking levels of investment in AI innovation.”

“Yet investors appear concerned that the flywheel is at risk of spinning out of control, in light of plateauing user growth and mounting pressure to better monetise existing audiences.”

Alex Brownsell, Head of Content at WARC Media

& co-author of the report

The user growth figures support that concern. Meta reports 3.5 billion daily active users across its family of apps, but Q1 produced the company’s first-ever decline in total DAUs, the result of restrictions in Russia and Iran. Latin America and Sub-Saharan Africa lead on high-net-worth engagement across Facebook and Instagram but generate far less revenue per user than North America or Europe. Meta is working on closing that gap; the rollout of Threads ads in Brazil is one signal of intent.

Campaign Performance

Meta’s Q4 2025 model rollout drove a 24% increase in incremental conversions through improved attribution. Analysis by Fospha found cost-per-purchase has improved 4.5% year-on-year. Brands using Meta’s Advantage+ tool are seeing 41% higher blended ROAS and 17% lower new customer acquisition costs compared with manual campaign management.

Creator-linked Partnership Ads are landing: 71% of consumers report making a purchase within days of seeing creator content on Meta’s platforms.

Short-form video is pulling both platforms in the same direction. Reels accounts for 45% of all engagement on Instagram; on Facebook, the figure is 29%, with time spent watching video up 8% quarter-on-quarter.

The Structural Question

The performance case for Meta is measurable and, for most advertisers, still persuasive. The strategic problem is bigger. WARC forecasts growth decelerating to 12.1% in 2027, still substantial but a marked slowdown. Whether advertising alone can sustain the AI investment Meta needs to stay competitive is a question its results have not had to answer. Investors are asking it anyway.