Netflix’s Ad Business Is No Longer a Side Project

WARC forecasts the streaming giant will take nearly 10% of global CTV ad spend by 2027 and that’s before any Warner Bros. Discovery deal.

Netflix spent years insisting it didn’t need advertising. Then it launched an ad tier and watched it grow faster than almost anything else in the business. Quietly, it dropped the modesty. The latest WARC Media Platform Insights report on Netflix makes clear that the company is now firmly in the advertising game. It’s playing to win market share, not just riding industry tailwinds.

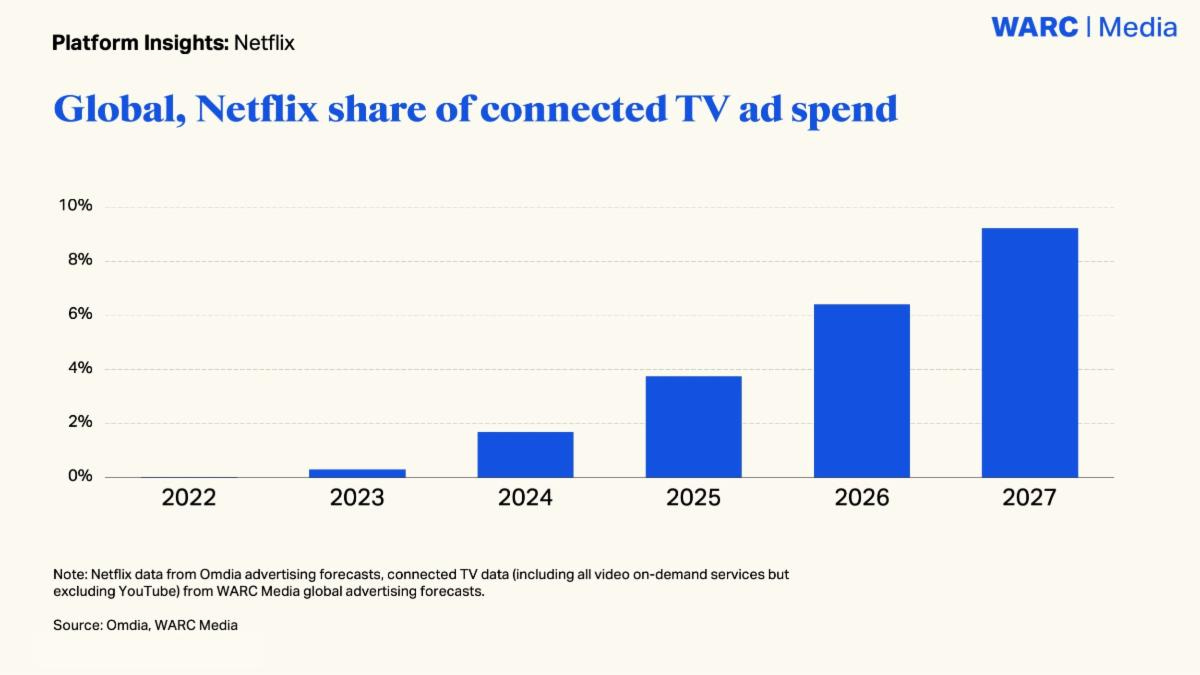

The numbers tell the story bluntly. Netflix generated more than $1.5bn in advertising revenue in 2025. That accounted for just 3.3% of its total income. According to Omdia data, that figure is set to double to $3bn this year, before reaching $8bn by 2030. For context, its share of global connected TV (CTV) advertising spend is projected to jump from 3.7% in 2025 to 9.2% in 2027. That’s not incremental growth. That’s a land grab.

What makes this significant for the advertising industry isn’t just the revenue trajectory. It’s about where Netflix is positioning itself in the competitive landscape. The company has publicly acknowledged YouTube as a direct competitor for TV viewing time. Five years ago, such a statement would have seemed almost absurd. Netflix’s response is to lean hard into what it calls ‘premium storytelling’. The bet is that curated, high-quality content commands a different kind of attention than the algorithm-driven, user-generated content that dominates YouTube’s viewing hours.

The CTV Opportunity

Connected television has been the growth story in advertising for several years. But the spoils have been unevenly distributed. Netflix is now moving aggressively to claim a bigger slice. The WARC data shows it’s targeting competitor share rather than waiting for the overall market to expand. This shows a more aggressive posture than the company has historically taken with commercial operations.

The potential acquisition of Warner Bros. Discovery, if it materialises, would significantly accelerate this. More content would mean more inventory and more engagement. It would also provide more data to sell advertisers on the quality of its audience. Netflix’s pitch to brands has always rested on the argument that viewers lean in rather than scroll past. A larger, more diverse content library makes it easier to sustain that case.

In the US market, the categories spending most on Netflix advertising in Q2 2025 were shopping ($82m), consumer-packaged-goods ($78m), financial services ($66m), travel and tourism ($54m), and telecoms ($44m). That’s a broad spread across high-value categories, which suggests advertisers are treating Netflix as a mainstream buy rather than a niche premium play.

The Audience Question

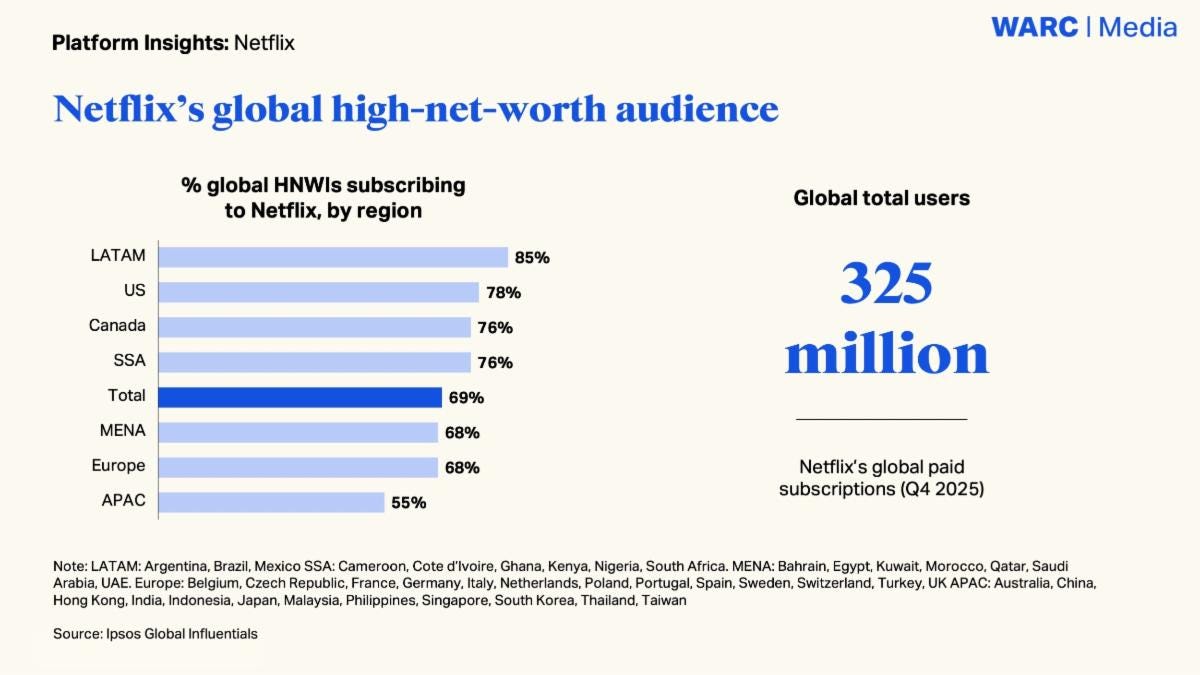

Scale matters to advertisers, and Netflix has it. Global paid subscriptions reached 315 million in Q4 2025. The company reports its total audience reach is approaching one billion, once shared households and non-paying viewers are included. Members are consuming 200 billion hours of content annually. In the UK, Netflix accounted for more than half of all subscription video-on-demand viewing last year.

The challenge — one the whole SVOD industry faces — is declining per-user viewing time. Younger audiences are especially likely to switch between Netflix and free platforms like YouTube. To respond, Netflix is extending beyond its core format. Video podcasts, music partnerships, sports livestreaming, and gaming integrations are in play. Each is designed to capture attention in the gaps that episodic drama and film don’t reach.

The live sports push is particularly worth watching. Sports rights are expensive, but they deliver appointment viewing. This type of content commands premium advertising rates and, crucially, drives subscription acquisition. Netflix has already made moves here. It’s reasonable to expect those bets to get larger.

What Advertisers Actually Think

The WARC report draws on Kantar data to assess how Netflix is perceived by brands, and the results are favourable. Netflix ranks fourth among global platforms for perceived trustworthiness, behind YouTube, Instagram and Google. It is also described as the only major platform with strict content curation. This is a genuine point of differentiation as brand safety on user-generated platforms remains a persistent concern.

Global consumers reportedly view Netflix ads as higher quality and more entertaining than those on other platforms. Dynamic and personalised formats are cited as drivers of that perception. Whether this will translate into performance metrics at scale is still a question advertisers will be pressure-testing over the next two years as Netflix’s ad business matures.

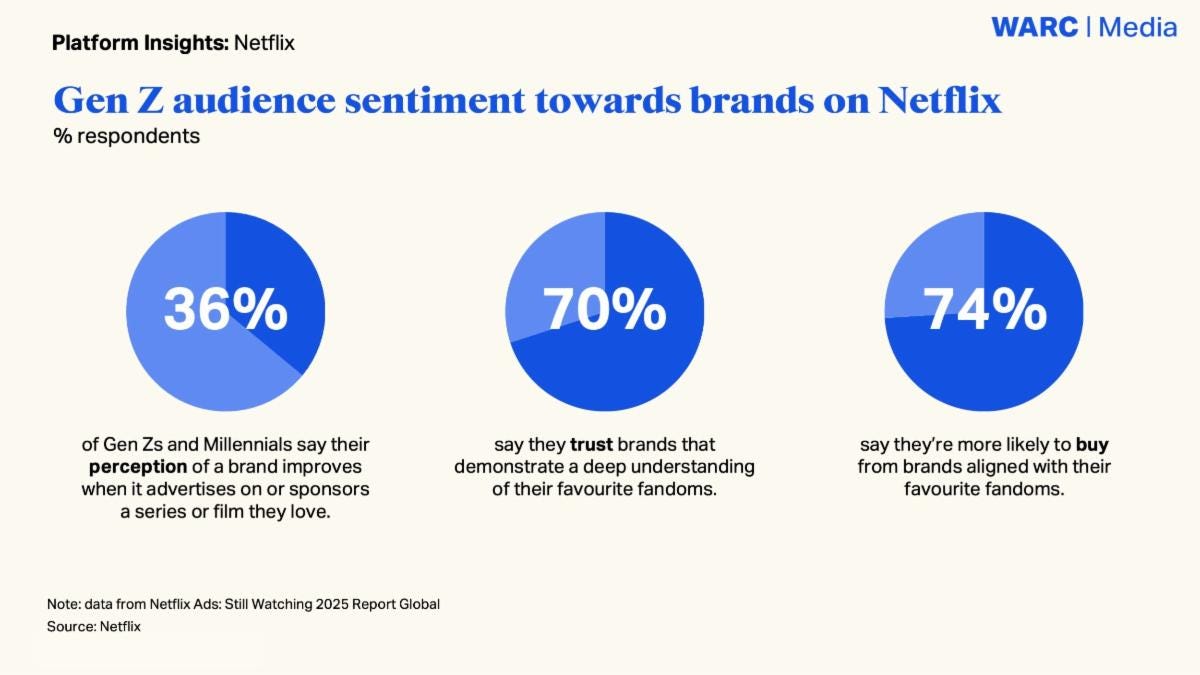

The Gen Z picture is interesting. WARC’s data suggests that 70% of Gen Z audiences are more likely to trust brands that align with their favourite shows. In addition, 74% are more likely to purchase from brands connected to fandoms they identify with. Netflix has built some of the most talked-about fandoms in popular culture — Squid Game, Stranger Things, and Wednesday. Brand integrations within those IP universes are a logical commercial extension. Younger consumers may be watching less Netflix than their parents. However, when they do watch, the affinity runs deep.

The Bottom Line

Netflix has moved from advertising sceptic to one of the most consequential players in the CTV market in a remarkably short time. The revenue forecasts are ambitious but they’re not implausible — the company has the audience, the content quality, and increasingly the advertiser relationships to support them.

For media buyers, the strategic question is no longer whether Netflix deserves a place on the plan. It’s how quickly its share should grow, and at whose expense. The obvious answer is that CTV budgets previously allocated to linear TV and to other streaming platforms will come under pressure. Netflix is making sure it’s the destination for those reallocated dollars.

The WBD acquisition question hangs over everything. If it happens, the scale of what Netflix could offer advertisers changes substantially. If it doesn’t, Netflix will have to build that scale through originals and live events alone. Either way, the advertising experiment is well and truly over. This is the main event.

Platform Insights: Netflix is part of a series of reports exclusive to WARC Media subscribers that explores platform trends through the lens of investment, user engagement and performance. This latest report follows other Platform Insights such as LinkedIn, Reddit, Amazon, TikTok, Spotify and Facebook.