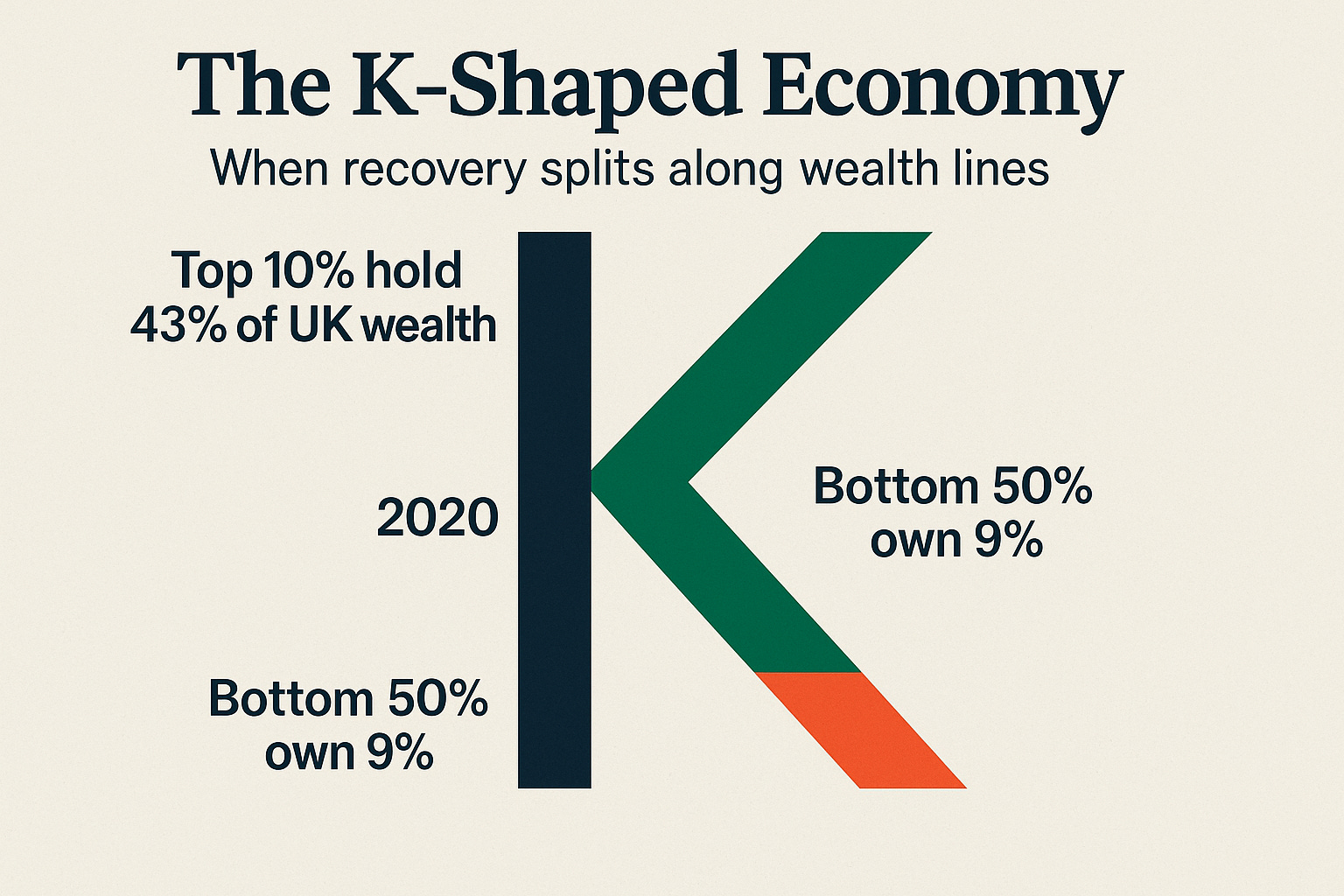

The K-Shaped Economy: When Recovery Splits Along Wealth LinesFrom Cannes Lions to corner shops, the economic divide reshaping marketing strategyThe Media StackNov 21, 2025∙ Paid21ShareContinue reading this post for free, courtesy of The Media Stack.Claim my free postOr purchase a paid subscription.PreviousNext